NEW YORK, 2014-04-16 — /Travel PR News/ — The hotel industry outlook for the top 25 North American Markets is showing an increase of 4.3% in committed occupancy for March 2014 – February 2015, based on group commitments and individual reservations on the books as of February 23, 2014 compared to the same time last year. The group segment is up 3.9% in room nights committed (contracted). New group business added over the last month (pace) are up 4.0% over the comparable period last year. Transient room nights booked are up 5.5% compared to the same time last year. Average daily rate (ADR) is growing slightly above occupancy, up 2.8% based on reservations currently on the books for 2014.

For the first quarter of 2014, overall committed occupancy is up 3.0% in the top 25 markets. Committed occupancy for the group segments is up 3.8% and the transient segment is up 2.6% compared to a year ago. Average daily rate for the first quarter is up 2.6% over the same time last year. Business segment ADR, which includes weekday transient negotiated and retail segments, is up 3.0%. Leisure segment ADR, which includes transient discount, qualified and wholesale segments, is up 3.2%.

2014 Forecast

I recently spoke to the audience at the Hunter Conference in Atlanta regarding the outlook for 2014. I provided an outlook for occupancy, ADR and RevPAR growth for the full year, based on what we are seeing in terms of year-to-date performance and, more importantly, based on advance booking performance for the coming months. I thought I would share this forecast with the readers of the TravelClick Perspective as well.

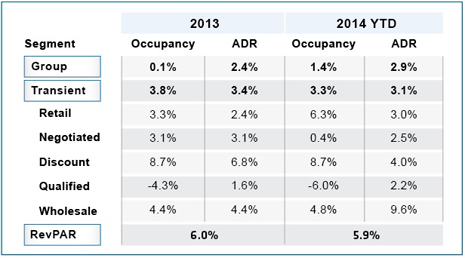

Let’s first look at year-to-date performance. Overall RevPAR performance so far this year is in line with what we saw for the full year 2013, as shown below:

However, we are seeing that so far this year, group is contributing slightly more and transient slightly less to RevPAR growth. Slower growth in the transient negotiated segment is a big factor in the lower overall transient segment growth. The particularly harsh winter experienced throughout much of the Northeast likely explains much of this negotiated segment weakness. Fortunately, the stronger performance of the group segment and the more leisure focused transient segments provided the support needed to maintain RevPAR growth.

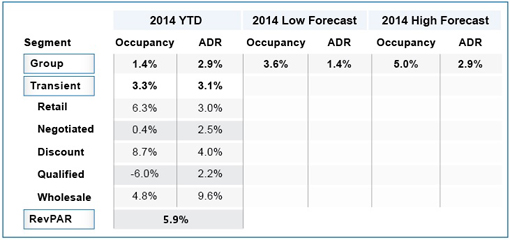

As we look forward to the balance of the year, we first look at the outlook for the group segment. Group business books well in advance of arrival. At this point in the booking cycle, more than 70% of the group room nights for 2014 are already contracted. This provides a strong indication of expectations of full year 2014 group segment performance. Based on that demand on the books, contracted group room nights are up 4.2% over the same time last year. Group ADR growth is more sluggish, down -0.4% versus last year. However, group ADR is based on group reservations against contracted blocks, not on contracted group sales. These reservations come in much closer to the arrival date, so our insight into ADR is more limited. Nevertheless, our expectations for group ADR growth are more tempered than what we are expecting for growth occupancy growth.

In addition to group business being ahead of last year by 4.2%, we have seen strong new group sales pace since the start of the year. New group room nights added in the first two months of the year for the balance of the year (March – December) exceeded last year’s new sales pace by 7.4%. This leads us to a rather bullish forecast for 2014 group segment performance, at least in terms of room night growth, as shown below:

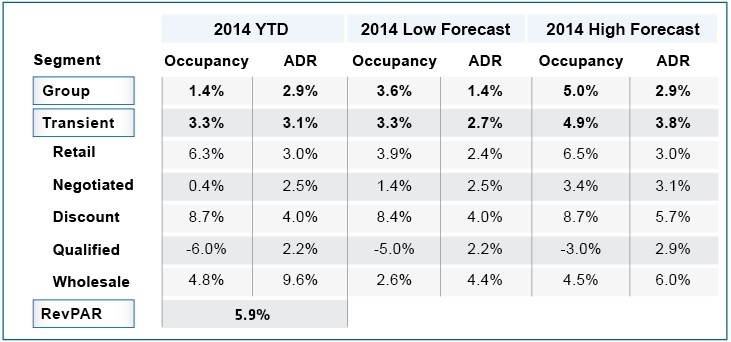

When looking at transient segment performance, we focus mainly on the three transient segments that comprise more than 80% of transient segment room nights: retail, negotiated and discount. Transient room nights on the books for the balance of 2014, for these three primary segments, are ahead of same time last year by 7.2%, 5.1%, and 8.0%, respectively. This demand pace is even with or ahead of both year-to-date and 2013 performance in each of these segments. The ADR outlook for the future months, based on the reservations on the books, is likewise as strong or stronger than year-to-date and 2013 performance. As a result, we expect continued strong transient segment performance for the remainder of 2014, as shown below:

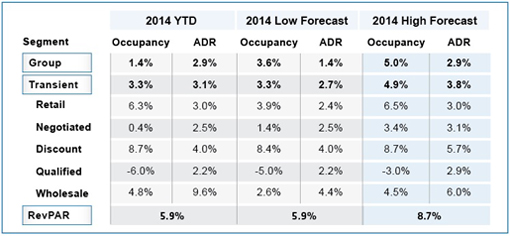

Based on the above forecasts for 2014 occupancy and ADR growth by segment, and the mix of business across these segments, we forecast RevPAR growth for 2014 to meet or exceed 2013 and year-to-date RevPAR growth:

Recent trends and advance booking strength bias our expectations to the high end of this range.

Performance Summary

The chart below shows the year-over-year position by market of committed occupancy, reserved occupancy, ADR, and revenue per available room (RevPAR), based on business on the books for the future 12 months. Committed occupancy is group blocks plus transient reservations. Reserved occupancy, ADR, and RevPAR are based only on reservations (group pickup and transient reservations). Shades of green indicate highest performance of the markets, while shades of orange indicate average performance, and shades of red indicate lowest performance.

TravelClick_Perspective_March_2014.pdf

About TravelClick, Inc.

TravelClick (TravelClick.com) provides innovative cloud-based solutions for hotels around the globe to grow their revenue reduce costs and improve performance. TravelClick offers hotels world-class reservation solutions, business intelligence products and comprehensive media and marketing solutions to help hotels grow their business. With local experts around the globe, we help more than 36,000 hotel clients in over 160 countries drive profitable room reservations through better revenue management decisions, proven reservation technology and innovative marketing. Since 1999, TravelClick has helped hotels leverage the web to effectively navigate the complex global distribution landscape. TravelClick has offices in New York, Atlanta, Philadelphia, Chicago, Barcelona, Dubai, Hong Kong, Houston, Melbourne, Orlando, Shanghai, Singapore and Tokyo. Follow us on twitter.com/TravelClick and facebook.com/TravelClick.

NEW DELHI, 2026-Mar-28 — /Travel PR News/ — For decades, Manali was the end of…

New York, New York, 2026-Mar-27 — /Travel PR News/ — Cape of Senses has been accepted into Virtuoso’s…

(NEWS) SHANNON, Ireland, 2026-Mar-26 — /Travel PR News/ — Passengers moving through Shannon Airport on Thursday…

(NEWS) MANCHESTER, UK, 2026-Mar-26 — /Travel PR News/ — For many travellers passing through Manchester Airport…

(IN SHORT) Hyatt Hotels Corporation has appointed Julienne Smith as Head of Americas Growth, tasking…

(IN SHORT) Park Hyatt Johannesburg, South Africa’s first Park Hyatt property, has been named one…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}